Forum Replies Created

-

AuthorPosts

-

We’re going to move to 31OCT expiration. Same strikes, same price – just 1 more day until expiration.

Order Ticket Type Asset Duration Strike C/P BTO SPX 31 OCT 17 2570 Call STO SPX 31 OCT 17 2565 Call STO SPX 31 OCT 17 2430 Put BTO SPX 31 OCT 17 2425 Put Total Credit: $0.80 I’m going to add a hedge here. 2575 Call delta is around 20 and that triggers this hedge. My NET delta in this trade is around -50. I am going to look to add 30 delta to reduce my NET exposure by 2/3. I am adding (3) ten delta calls in the same expiration cycle.

Order Ticket Type Asset Duration Strike C/P BTO SPX 17 NOV 17 2600 Call Total Debit: $2.60 We’re going to roll up 2390/2380 Bull Put spread up to 2460/2450 for a credit.

Order Ticket Type Asset Duration Strike C/P STO SPX 17 NOV 17 2460 Put BTO SPX 17 NOV 17 2450 Put BTC SPX 17 NOV 17 2390 Put STC SPX 17 NOV 17 2380 Put Total Credit: $0.45 – $0.50 I’m going to stop out of this trade here. My target was .60c per contract and my stop is 2X my profit target.

Order Ticket Type Asset Duration Strike C/P STC SPX 31 OCT 17 2570 Call BTC SPX 31 OCT 17 2565 Call BTC SPX 31 OCT 17 2430 Put STC SPX 31 OCT 17 2425 Put Total Debit: $2.00 I’m going to roll up 2575/2585 Bear Calls spread and take off the OTM call hedge

1. Roll up Bear Call spread

Order Ticket Type Asset Duration Strike C/P Buy To Open SPX 17 NOV 17 2610 Call Sell To Open SPX 17 NOV 17 2600 Call Sell To Close SPX 17 NOV 17 2585 Call Buy To Close SPX 17 NOV 17 2575 Call Total Debit: $1.90 2. Close out the hedge

Order Ticket Type Asset Duration Strike C/P Sell To Close SPX 17 NOV 17 2600 Call Total Credit: $4.40 SPX at 2553

VIX at 9.93I’m going to put on an Iron Condor in 15 DEC expiration cycle with 63 days until expiration. I’m using regular monthly expiration cycle. I’m selling:

SPX 2440/2430 Bull Put spread

SPX 2640/2650 Bear Call spreadShort strike on the put side has a delta around 17 and the short call delta around 11.

These are 10 point wide credit spreads.Risk Profile:

My Max Allowable Loss (MAL) is around 1.5 times total credit. If total credit is $1.70 then MAL is $2.55

Our first profit target is 50% of credit in 25 days or less.

We’re going to manage this position when short put delta reaches 25 or short call delta crosses 20Order Ticket Type Asset Duration Strike C/P Buy To Open SPX 15 DEC 17 2650 Call Sell To Open SPX 15 DEC 17 2640 Call Sell To Close SPX 15 DEC 17 2440 Put Buy To Open SPX 15 DEC 17 2430 Put Total Credit: $1.70-$1.80 I’m going to put on an Income Calendar in Russell 2000 (RUT) centered around 1510. I am using puts to establish this position. I am selling 1510 put in 10 NOV expiration cycle and I am buying 1510 put in 24 NOV expiration cycle. This trade is done for a debit because the option that we’re selling has less time premium than the option that we’re buying. I am looking to add another calendar centered around 1530 strike IF/WHEN RUT trades to 1530. I am looking to make around 15% return on margin for this trade and I don’t want to risk a lot more than what I’m looking to make.

Risk Profile

Order Ticket Type Asset Duration Strike C/P Sell To Open RUT 10 NOV 17 1510 Put Buy To Open RUT 24 NOV 17 1510 Put Total Debit: $5.00 I’m going to put on an Income Trade in RUT with about 60 days to expiration. I am buying a slightly OTM broken wing put buttefly with 50pt wing on the downside and a 40pt wing on the upside. I’m going to center this butterfly at 1490. My profit target is around 10-15% return on margin and I dont want to risk a lot more than what I am looking to make. I will add to this trade as RUT trades above 1530 and if RUT continues above 1560, I will look to add one more (3rd) butterfly. All additional butterflys will be 30pt apart.

Tier 1:

Buy 1440 Put

Sell 2X 1490 Put

Buy 1530 PutOrder Ticket Type Asset Duration Strike C/P BTO RUT 15 DEC 17 1530 Put STO X2 RUT 15 DEC 17 1490 Put BTO RUT 15 DEC 17 1440 Put Total Debit: $6.40 Risk Profile:

AnonymousWhy don’t you do some trades with about 15 days to expiration.

Trades that are closer to expiration are very sensitive to price movement (Gamma). In this trade, I’m looking to hold this butterfly for about a month and I’m taking advantage of time decay. If RUT makes a big move it’ll hurt the position, and IF I have just 2 weeks to expiration then I will have no time to make any adjustments and will have to take a loss.

You can also compare a 14-day butterfly and a 60-day butterfly. Look at the steepness of the T+0 line, a move outside of the tent will be felt a lot more in the 14 day fly because it is closer to expiration. Again, my goal is to hold it for as little as possible and keeping the T+0 line as smooth as possible will help me prevent taking a big loss.

14DTE:

60DTE:

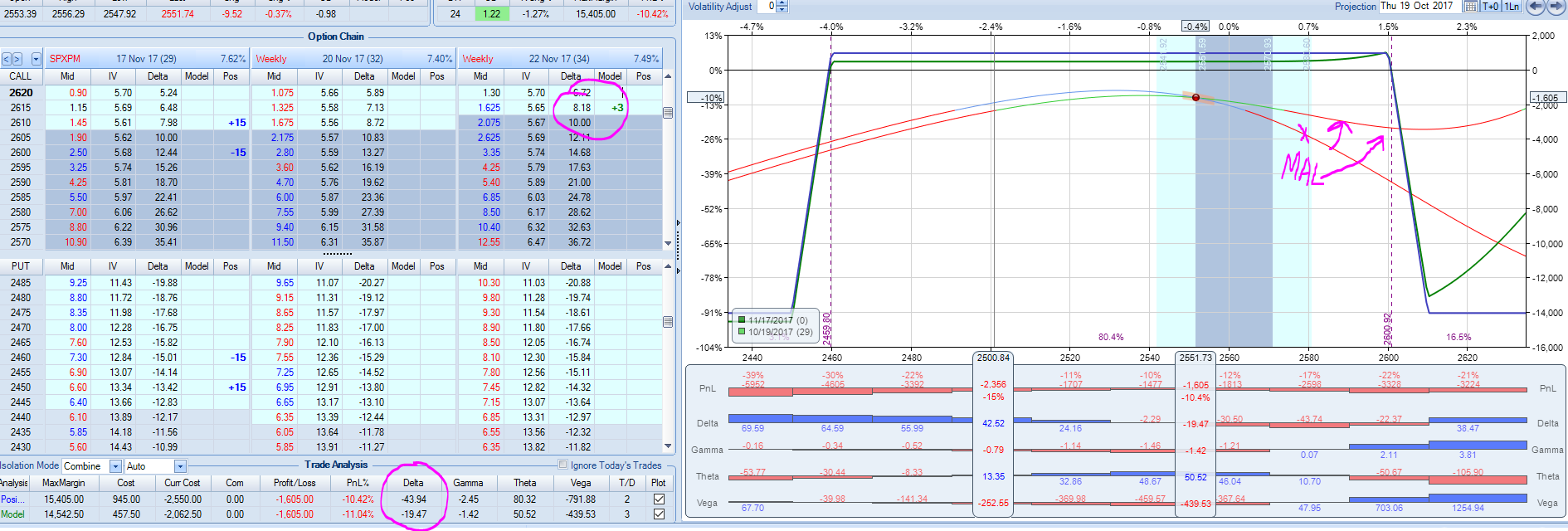

SPX is pulling back to 2551 today and I’m going to make a small adjustment here. I’m looking to cut my NET delta by about 50% here and this will push my MAL or stop on the upside higher up in price. My current NET delta is around -44 and I want to add about 20-25 delta to this trade. To add 20 delta, I can use two 10 delta calls, one 20 delta call, three 7 delta calls….

I’m going to pick up 22NOV 2615 Calls that are delta 8

P/L graph:

Order Ticket Type Asset Duration Strike C/P Buy To Open SPX 22 NOV 17 2615 Call Total Debit: $1.60 I’m going to take this trade off for a profit after being in it for 12 days.

P/L graph:

Order Ticket Type Asset Duration Strike C/P Buy To Close RUT 10 NOV 17 1510 Put Sell To Close RUT 24 NOV 17 1510 Put Total Credit: $5.50 Trade SetUp:

We’re going to put on an Iron Condor in ADBE with 50 days to expiration. We’re selling options around 12 delta and buying options 5 points farther OTM. We’re looking for a credit of .75c per 1 Iron Condor. We will not make adjustments to this trade and we’ll take this trade off at a loss of 2X credit.

P/L graph:

Order Ticket Type Asset Duration Strike C/P Buy To Open ADBE 15 DEC 17 200 Call Sell To Open ADBE 15 DEC 17 195 Call Sell To Close ADBE 15 DEC 17 155 Put Buy To Open ADBE 15 DEC 17 150 Put Total Credit: $0.75 I’m going to tighten up this Iron Condor on the put side take in a slightly bigger credit. I’m moving Bull Put spread from 155/150 up 5 points to 160/155 and mid price for this IC is between 0.90-0.95c

P/L graph:

Order Ticket Type Asset Duration Strike C/P Buy To Open ADBE 15 DEC 17 200 Call Sell To Open ADBE 15 DEC 17 195 Call Sell To Close ADBE 15 DEC 17 160 Put Buy To Open ADBE 15 DEC 17 155 Put Total Credit: $0.90 – $0.95 Risk Management is the same, I will risk 2X credit for this trade and my first profit target is 50% of max credit in 50% of time to expiration.

We’re going to make an adjustment on the upside, as planned:

Order Ticket Type Asset Duration Strike C/P Buy To Open SPX 15 DEC 17 2665 Call Total Debit: $2.80 -

AuthorPosts