The Black Swan

Everyone has at least heard of the term Black Swan event, but what is it really and how can one react to it financially. Before we begin let’s first understand what a Black Swan event is.

Black swan theory was developed by Nassim Nicholas Taleb. Without going into too much detail, a black swan event can be identified by three common traits.

- The event is a surprise (to the observer).

- The event has a major effect.

- After the first recorded instance of the event, it is rationalized by hindsight, as if it could have been expected; that is, the relevant data were available but unaccounted for in risk mitigation programs.

Although there are lots of examples of such events, let’s look at a more recent one.

What we saw in early 2018 could be described as a Black Swan event. We had several vol arb firms forced to cover their short vol positions and that caused the demand for VIX options to go through the roof. Here’s a chart of $VVIX which is the VIX for the VIX, it measures the demand for VIX options:

Fast forward to today (early Aug 2018) and demand for VIX options is at the lowest level since August 2017. Anyone with long exposure to the market, IRA, 401K would feel that this is a good time to buy some sort of protection in case the volatility picks up and the market starts to head south. We’re not talking about a 5% correction over the next few months, we’re talking about a big, fast move to the downside.

Black Swan Protection

Obviously, there are many different ways one could try to protect themselves from a Black Swan event. One popular way is to buy protection against this type of event is to go out and buy some VIX calls. Before we go down this road it is important to first understand how VIX options work. Instead of reinventing the wheel, let me refer you to a write-up that clearly defines VIX options.

Chris from Projectoption.com wrote about VIX options in detail:

Options on the VIX are European-style, which means they can’t be exercised until expiration. Additionally, they’re cash-settled, as the VIX doesn’t have tradable shares that can be purchased or sold by exercising. So, if you own a 15 call on the VIX and the VIX Index spikes to 30, you can’t exercise your option to buy VIX shares at 15 to sell them at 30. Instead, your P/L is determined by where 30-day implied volatility is expected to be on VIX settlement day, which is represented by the corresponding VIX futures price.

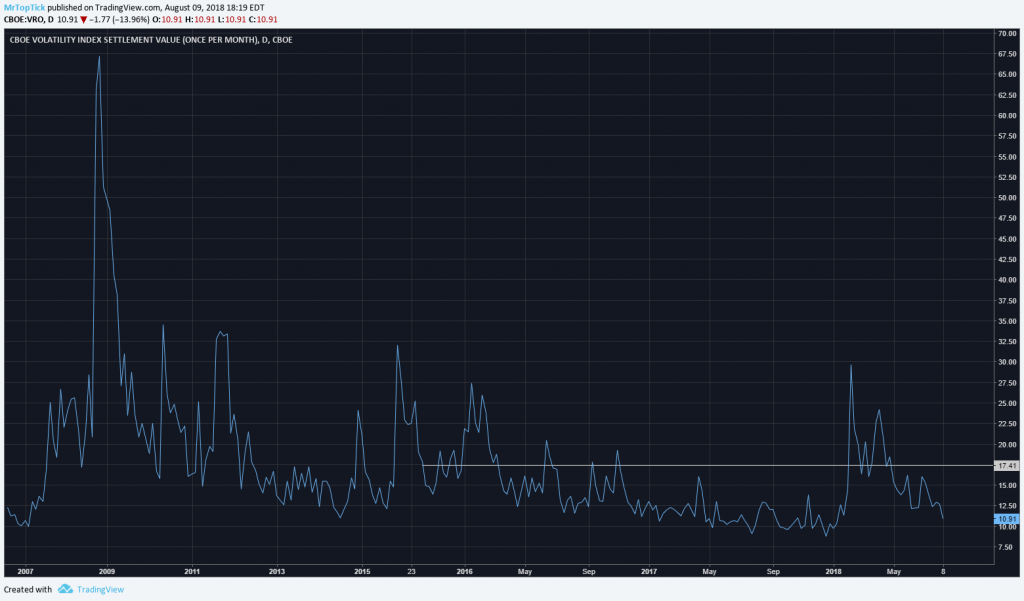

In other words, if you’re going to buy VIX options, you have to look at the VIX futures to understand how much premium you’re going to pay and where VIX needs to settle in order to make money on those options. Let’s consider this example. We go out and buy NOV 15 calls that are trading at $2.40. This means that the VIX needs to settle at 17.40 for these calls to be at break-even. Here’s the chart of VRO, the VIX settlement value:

Looking at this chart, it’s obvious that we’d need to see the kind of price action that we saw earlier this year to get above that 17.40 level. If the market stays in a range, trades higher or slightly lower, we could assume that we’re going to lose most, if not all of the premia we’d pay for those NOV 15 calls. So even though we did have our protection we were forced to pay for it and lost.

If we were to continue in this scenario where no event occurred, we would find a steady outflow of losses as we keep buying more and more calls for protection.

At some point, the continuous losses on the calls that are expiring worthless would eat into our gains and have a negative impact. So now comes the question:

Is there a way to put on the same kind of protection and not lose the premium?

To answer this question let’s consider this example:

Looking at the chart of $VRO, the VIX hasn’t settled below 10, except once and this was during the lowest volatility market since forever.

I would consider selling JAN 12 Put for $0.40 and buying JAN 20/24 Call spread for $0.40. My NET cost would be $0. The risk is on the downside if the VIX settles at $10 then my short 12 Put is $2.00 in the money. That’s a loss of $200 per contract. If you are wondering about holding naked puts short, with the liquidation of XIV and other short vol funds getting blown out earlier this year, the odds of seeing the kind of low volatility environment are pretty low.

On the flipside, if the VIX explodes here’s what the risk profile of this set up looks like:

Of course, markets are unpredictable, so here are the potential outcomes depending on market conditions:

- The market goes higher while the VIX stays above 12 – this trade makes nothing and loses nothing. The short put expires worthless and the long call spread expires worthless as well, but we had our protection in place and were able to sleep well at night.

- The market tanks hard and the VIX spikes to over 20 – this trade will help offset losses from long market exposure (remember the IRA, 401K, long-term investments?)

- The market goes parabolic, the way it did at the beginning of 2018 and the VIX settles at $10 – this trade will lose $200 per 1 contract.

In conclusion, I feel that selling a put to buy an OTM calls spread is a better way to structure a Black Swan protection trade than just going out and buying OTM VIX Calls. This way I don’t have to lose the premium I’d have to pay to buy the VIX 15 Calls. By selling a put to buy an OTM calls we still get the protection we are looking for without having to book constant losses as the calls expire worthless.

Once again, if you are wondering about holding naked put short, with the liquidation of XIV and other short vol funds getting blown out earlier this year, the odds of seeing the kind of low volatility environment are pretty low.

Once again this is just another idea and tool one can use to help safeguard their investments and financial future.