Iron Condor Adjustments is a very important topic.

Iron Condor adjustments are just as important as entry and exit.

One of the best strategies for traders that don’t want to chase the market or guess which way the market moves next is an Iron Condor.

This options trading strategy profits if the underlying stock remains within a specified range. What hurts this strategy is when the underlying stock makes a big move in either direction before the expiration date of this strategy. Sometimes, even with the underlying stock making a big move, it is possible to make a profit with this strategy. Other times, this trade needs to be either adjusted or closed out for a loss. I’m a big believer that any adjustments to this trade need to be planned before the trade is actually put on. One thing you don’t want to do is to close your eyes and hope that the underlying stock goes back to where it was and that this trade will somehow make a profit. High probability Iron Condors can lose a lot more than they can make, and it is very important not to let a small loser turn into a big ugly one.

Before we take a look at a few different ways Iron Condors can be adjusted, let’s take a look at Iron Condor features.

An Iron Condor involves selling a Bull Put spread and a Bear Call spread simultaneously. This strategy has a limited risk and a limited profit risk profile. The most Iron Condor can make is the credit received for selling

- Do NOTHING. This is probably the worst thing anyone can do. Just sit there and convince yourself that the underlying is going to come back and this trade is going to be a winner. Next thing you know, the underlying is trading outside of the short option’s strike price and now this trade is close to being down 50%. At this point, the only thing that can be done to avoid taking a full loss is to roll the troubled side of the Iron Condor up (or down) in price.

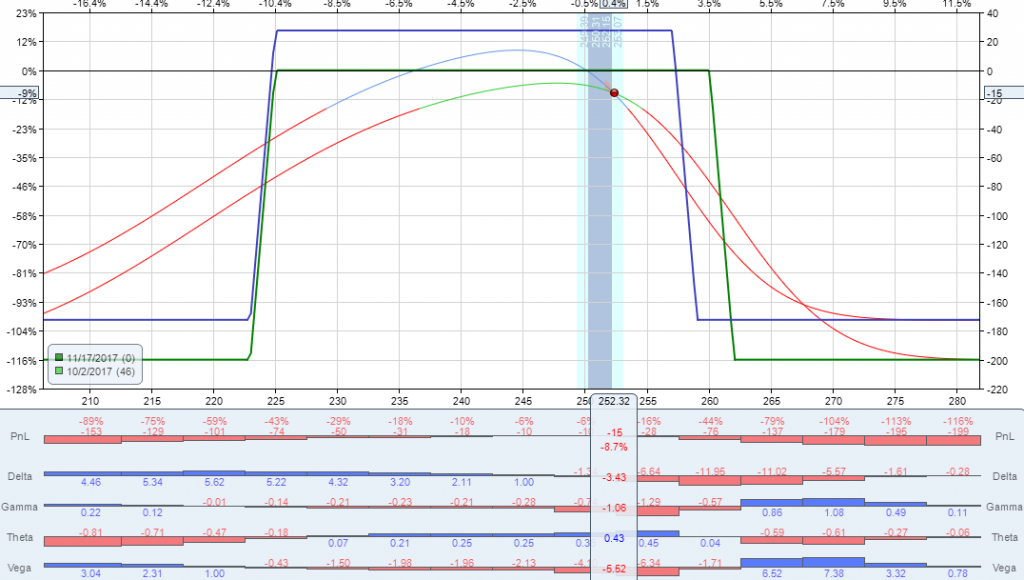

- Roll Up or Down. This adjustment will require you to spend most if not all of the credit that was received when this trade was initiated. The best case scenario for this trade is that the troubled spread is moved up or down in price and the underlying expires somewhere inside of short strikes and this trade becomes a break even or a small loser. For example, let’s take a look at an Iron Condor in SPY with short strikes at 225 on the put side and 257 on the call side. Over the next 25 days, the underlying moved 6 points to the upside and the trade was showing a loss of about 8%. If the call spread was closed and re-opened at higher strikes, this adjustment would cost the entire credit that was collected to initiate the trade and the best case for this trade is that it’ll be a breakeven trade.

That’s when most traders decide to roll not just in terms of price, but out in time.

That’s when most traders decide to roll not just in terms of price, but out in time. - Roll Up or Down AND Out. This adjustment is made by rolling the troubled side of the Iron Condor farther away from where the underlying stock is trading AND farther out in time. For example, using the same Iron Condor set up, if the call spread is moved from November out to December and the strikes are moved from 257 to 263 and the put spread is moved from November to December and from 225 to 229 (keeping the same 2 point width of the spreads) then this adjustment will cost about 70% of initial credit and the duration of this trade will be extended another 30 days. This is what

adjusted risk profile would look like:

At this point, this trade has a very small profit potential relative to the amount of risk involved and the duration of this trade went from 46 days to 74 days.

- Delta Hedge. Another Iron Condor adjustment is to use NET delta to hedge this position. This is one of my favorite adjustments because by removing some of the directional exposure, this buys me time to wait and see how I need to adjust this position further. To hedge an Iron Condor using Delta I can use stock or options of the underlying instrument. Let’s say my NET delta of an Iron Conor is -20. I can buy 20 shares of the underlying to cut my NET delta to 0 OR I can buy two 10 delta calls that will add a total of 20 positive

delta and will neutralize my directional exposure. If the underlying continues to move against my position, I will then remove my hedge and roll up or down the troubled spread farther away from where the underlying is trading. By using a hedge for this adjustment, it helps to make up some of the losses accumulated by either short spreads of an Iron Condor. Here’s anexample how I use OTM options to hedge my Iron Condors: - Take a Loss. This is the part that most Iron Condor traders have a hard time with. Instead of cutting losses and preserving capital they start to look for reasons to stay in the trade. The price moves further against this position and then a smaller loss turns into a large loss and the trader ends up giving back most, if not all of the profits from previous winning trades. The key is knowing when to pull the plug. I always have a set number where I am going to cut the trade and move on.

These are the 5 ways that Iron Condors can be adjusted. I hope you find this information useful and if you have any questions or comments, feel free to reach out to me: igor@mrtoptick.com

Igor: I have been successful occasionally in mitigating some of the loss incurred in rolling out one leg, and, if the credit/risk balance is ok, rolling up the other leg for a net credit to help offset the roll up premium. I have a bias for bull spreads and usually set the put side first in the 25-30 delta range.

Ted,

That works too. I try my best to avoid rolling out in time. I find it easier to set a Max Allowable Loss for my trades and if I hit that point, I will take a loss and move on to the next set up.

Thanks for sharing.

Igor, I am new here on your website.

I was reading in the blogosphere that (at least simple) rolling down or up your combo are, on average (using past years backtesting), not such a great idea on SPX.

Have you tried to backtest your roll up or down rules above?

One more question, if I may. What is the software that you are using in this post/video?

Many thanks,

Francesco

Great question,

Rolling up or down, while doing high probability Iron Condors, isn’t the best adjustment because the credit received often won’t cover the cost of the roll.

I like to use OTM options to reduce my directional exposure when underlying starts to move towards one of my short strikes and then using profits from the hedge to help pay for the cost of the roll.

I am also not a big fan of rolling out further out in time because that will require more time in the trade and will start to deplete psychological over time.

I am a big fan of having a plan for each trade. Setting Profit Targets and Stop Losses or Max Allowable Loss points and if either is hit, I exit the trade.

The software I use to manage my trades is OptionNetExplorer.

Hope this helps.

Thanks for this information! It helped me turn a potential disaster into a manageable loss.

Hi..That was really a great article. Can you please guide on how do you go about target and stop loss for Iron Condor.

Garry, thanks for your question.

I usually set a stop and profit target before I enter the trade. I want to know as much information as possible before I get into the trade. This allows me to just follow the plan once I’m in the trade.

I normally set a stop at 1.2X – 1.5X credit received and start to defend the position when my short strike delta doubles.

My typical profit target is:

1. 50% of Max Profit

2. 70% of Max Profit

You’re welcome, Joe!

Hi, Igor,

Great article.

I have a question regarding delta hedges.

You mentioned “If the underlying continues to move against my position, I will then remove my hedge and roll up or down the troubled spread farther away from where the underlying is trading.”

So, for example, suppose, like this past Monday with the market going down, the short strike delta reaches 25 or 30, and I take out a delta hedge (buy a put whose delta equals half of the position net delta). Then, like this week, the market turned around quickly. Is this when you remove the hedge, by selling the put? In other words, while the put hedge is in effect, do you keep monitoring delta of short strike, to determine when to remove the hedge?

Thanks,

Mike

Hello Igor, Thanks for explaining the anatomy of Delta Hedging using OTM Options for Iron Condors. Can you please share some of your adjustments for “Iron Butterfly”? How to apply Delta Hedging using OTM Options for Iron Butterfly?